Accounting looks simple on paper—until a customer sends goods back. Suddenly, revenue must be reversed, inventory adjusted, and financial statements corrected. That’s where the sales return journal entry becomes critical. Done correctly, it keeps your books clean. Done poorly, it distorts profit, tax reporting, and financial analysis.

Whether you’re a business owner, accounting student, or finance professional, understanding the mechanics and impact of a sales return journal entry is essential. It’s not just a bookkeeping task. It’s part of revenue recognition, inventory management, and internal control.

Let’s walk through seven powerful insights that explain how to record, analyze, and manage sales returns accurately.

What Is a Sales Return Journal Entry?

A sales return journal entry records the transaction when a customer returns previously purchased goods. In accounting terms, it reverses part or all of the original sales transaction.

This typically affects:

-

Revenue accounts

-

Accounts receivable

-

Cash (if refunded immediately)

-

Sales returns and allowances

-

Inventory (if goods are resalable)

-

Cost of goods sold

Sales returns fall under contra revenue accounts. That means they reduce gross sales to arrive at net sales.

Understanding this concept is foundational in financial accounting.

Why Sales Return Journal Entries Matter

Sales returns are not rare exceptions. In industries like retail, e-commerce, wholesale distribution, and manufacturing, returns are routine. However, improper accounting treatment can cause:

-

Overstated revenue

-

Misleading profit margins

-

Incorrect tax calculations

-

Distorted financial statements

-

Poor financial reporting accuracy

In short, accurate bookkeeping protects financial integrity.

Now let’s break down the seven essential insights.

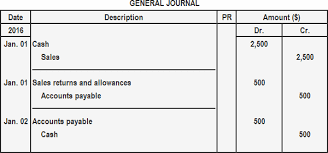

1. Understand the Double-Entry Impact

Every sales return journal entry follows the double-entry accounting system.

If the Sale Was on Credit:

When goods are returned:

Debit: Sales Returns and Allowances

Credit: Accounts Receivable

If inventory is returned in sellable condition:

Debit: Inventory

Credit: Cost of Goods Sold

This ensures both revenue and cost adjustments are properly recorded.

If the Sale Was for Cash:

Debit: Sales Returns and Allowances

Credit: Cash

And again, adjust inventory and COGS if goods are restocked.

The key principle: reverse both the revenue and the expense impact.

2. Sales Returns Reduce Net Revenue

A common mistake is treating returns as regular expenses. They are not.

Sales returns belong in a contra revenue account called “Sales Returns and Allowances.” This account reduces total sales to calculate net sales:

Net Sales = Gross Sales – Sales Returns – Discounts – Allowances

This distinction matters in:

-

Income statements

-

Revenue recognition analysis

-

Financial ratio calculations

-

Profit margin assessment

Proper classification improves financial statement accuracy.

3. Inventory Must Be Adjusted Carefully

Not every returned item goes back into inventory. Some may be damaged, obsolete, or unsellable.

If goods are:

Resalable → Increase inventory

Damaged → Record loss or write-off

Refurbishable → Record adjustments based on policy

Inventory valuation methods such as FIFO, LIFO, or weighted average cost also affect how the sales return journal entry is calculated.

This is where accounting judgment matters.

4. Tax and Compliance Considerations

Sales tax adjustments must accompany returns. If tax was charged on the original sale, it must be reversed proportionally.

Failure to adjust tax liability correctly can result in:

-

Overpayment

-

Audit discrepancies

-

Compliance penalties

Businesses operating in multiple jurisdictions must also consider regional tax laws.

In addition, proper documentation is crucial for audit trails and internal controls.

5. Timing Impacts Financial Reporting

Timing of the sales return journal entry affects reporting periods.

For example:

If goods are sold in December but returned in January, which accounting period reflects the return?

Under accrual accounting principles, returns are recorded when they occur. However, businesses may estimate expected returns during year-end adjustments.

This is especially common in industries with predictable return patterns.

Accurate timing ensures:

-

Revenue recognition compliance

-

Transparent reporting

-

Consistent accounting policies

6. Use Clear Documentation and Controls

Strong internal controls reduce fraud and errors.

Every sales return journal entry should be supported by:

-

Return authorization forms

-

Credit memos

-

Customer communication records

-

Inventory inspection reports

-

Accounting approval workflows

Without documentation, businesses risk revenue manipulation or inventory shrinkage.

Accounting transparency protects both management and stakeholders.

7. Monitor Return Trends for Strategic Insight

Sales returns aren’t just accounting entries—they provide operational intelligence.

High return rates may signal:

-

Product quality issues

-

Shipping damage

-

Incorrect product descriptions

-

Customer dissatisfaction

-

Pricing problems

Finance teams should collaborate with operations and marketing departments to analyze return data.

Tracking metrics such as:

-

Return percentage

-

Refund frequency

-

Product defect rates

-

Customer behavior patterns

can improve profitability and customer satisfaction.

Practical Example of a Sales Return Journal Entry

Let’s consider a scenario.

A company sells goods worth $1,000 on credit. The cost of goods sold is $600. Later, the customer returns the goods.

Entry to Record Return:

Debit: Sales Returns and Allowances – $1,000

Credit: Accounts Receivable – $1,000

Debit: Inventory – $600

Credit: Cost of Goods Sold – $600

This restores inventory and reduces revenue.

Notice how both revenue and cost are adjusted. That’s the power of double-entry bookkeeping.

Key Differences: Sales Returns vs Allowances

Sales returns involve physical goods being returned. Sales allowances occur when customers keep goods but receive partial refunds due to defects or dissatisfaction.

Both reduce revenue, but only returns typically affect inventory accounts.

Understanding this distinction ensures precise financial reporting.

Impact on Financial Statements

The sales return journal entry affects:

Income Statement

-

Reduces gross sales

-

Impacts net income

Balance Sheet

-

Decreases accounts receivable or cash

-

Adjusts inventory

Cash Flow Statement

-

Reflects refund outflows (if cash sale)

These adjustments influence financial ratios such as:

-

Gross profit margin

-

Net profit margin

-

Inventory turnover

-

Return on assets

Even small errors can distort financial performance analysis.

Common Mistakes to Avoid

Here are frequent accounting errors:

-

Forgetting to adjust cost of goods sold

-

Misclassifying returns as expenses

-

Ignoring tax reversals

-

Delaying entries until month-end

-

Failing to document return authorization

Avoiding these pitfalls improves bookkeeping accuracy and audit readiness.

Sales Return Journal Entry in Modern Accounting Systems

Most accounting software automates sales return journal entry recording. However, automation does not eliminate the need for understanding.

ERP systems integrate:

-

Inventory tracking

-

Revenue management

-

Tax adjustments

-

Customer account reconciliation

Still, accounting professionals must review entries for accuracy and compliance.

Technology assists—but expertise ensures correctness.

Strategic Importance Beyond Bookkeeping

At a strategic level, sales return data influences:

-

Product development

-

Customer experience improvements

-

Supply chain optimization

-

Quality control systems

-

Pricing strategies

In fact, businesses that analyze return behavior often uncover operational inefficiencies that directly impact profitability.

Returns are signals. Smart companies listen.

How to Improve Sales Return Management

To reduce excessive returns and improve financial stability:

-

Strengthen quality control

-

Improve product descriptions

-

Enhance customer support

-

Use accurate inventory management systems

-

Establish clear return policies

Financial management is not just reactive. It’s preventive.

By minimizing return rates, businesses protect revenue and improve operational efficiency.

Final Thoughts

The sales return journal entry may seem like a routine accounting process. However, its impact reaches far beyond bookkeeping. It influences revenue accuracy, inventory valuation, tax compliance, financial reporting, and business strategy.

Understanding how to record a sales return journal entry correctly ensures:

-

Transparent financial statements

-

Accurate net sales calculations

-

Proper inventory adjustments

-

Compliance with accounting standards

-

Strong internal controls

If you manage accounts, run a business, or study accounting, mastering this concept is non-negotiable.

{kind=link}